“I wish I knew this stuff in my 20s!”

This is one of the most common phrases I hear as a financial planner. By the time that we buckle down and take control of our money, we realize how beneficial these skills would have been in our 20s and 30s.

Let’s give our schools a break though!

Between learning the periodic table…

And learning how to complete a work cited page…

There just wasn’t much time left to devote to those little details of learning how to like, you know, make responsible financial decisions.

That being said, here are five things that I wish I would have learned in high school

#1 The Magic of Compounding Interest

Yes. It’s magic.

I believe that one of the best things that you can give someone to motivate them is perspective. Compounding interest gives young people one HUGE advantage over their older, and often-times better-paid peers. That advantage is time.

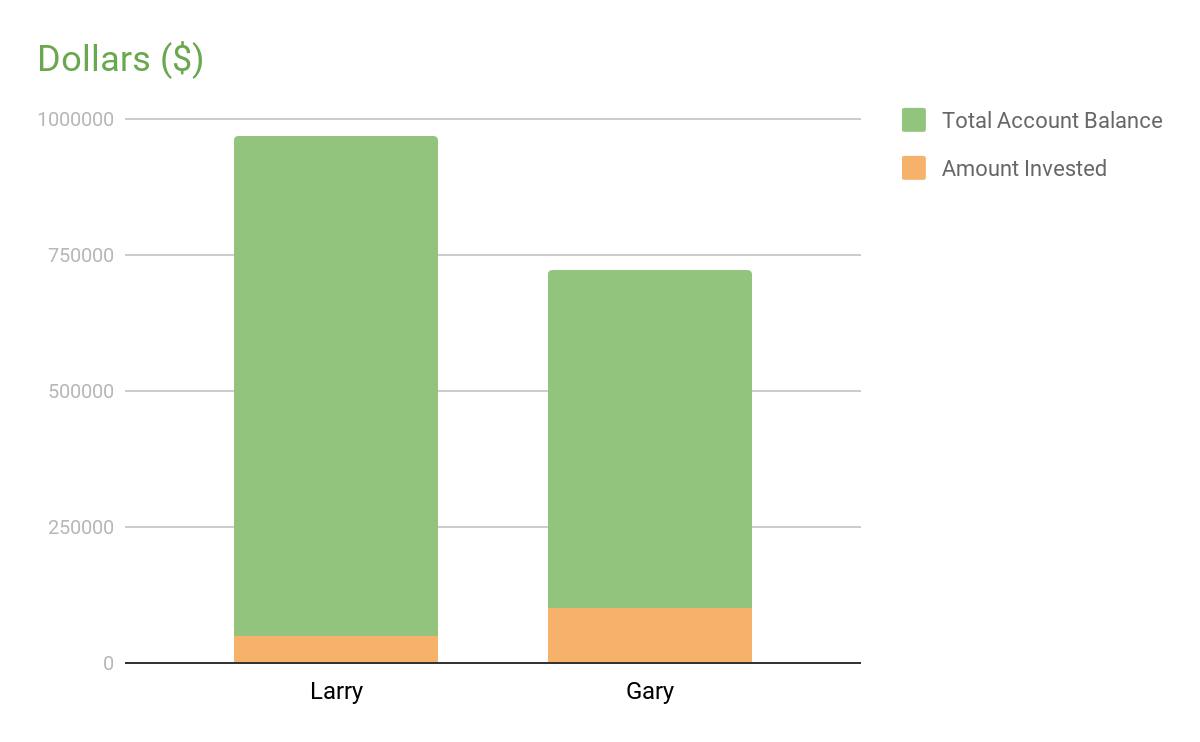

Let’s look at the example of two friends and college classmates, Larry and Gary.

Larry graduates college, gets a job, and then starts saving $5,000 per year to his retirement account right away at age 22. Let’s assume his investments grow at 8% per year on average.

He saves the same amount for the first ten years but then stops saving altogether when he turns 32.

Gary, on the other hand, got a similar job to Larry, but he spent the first ten years out of college spending everything he made. At age 32 Gary realizes it’s time to get focused.

He then begins saving $5,000, and he does this for 20 years, from age 32 until age 52, before he stops saving. Let’s assume that his investments also grow at 8% per year.

So here are the facts – Larry has invested a total of $50,000; Gary has invested a total of $100,000. Both grew at 8% per year on average.

Now let’s assume that both retire at age 65. Who do you think has more money at that point?

It’s gotta be Gary, right? The guy invested twice as much.

Wrong! Larry has more money! Based on the compounded growth of 8% per year then by the time that both of them are 65 years old, Larry would have $918,162 in his investment account while Gary would have just $622,277 in his.

To take it a step further, let’s assume that Larry never stopped saving $5,000 per year after turning 32. If he grew at 8% per year then by the time that he turned 65 he would have $1,647,915 in his investment account.

Now, what if instead of saving exactly $5,000 each and every year, let’s assume that Larry actually gets some raises in his lifetime and he applies part of each raise to his annual investment.

If he increases the amount saved by 3% per year (i.e. in year one he saves $5,000; in year two he saves $5,150, etc…) then by the time that he was 65 he would have $2,588,452 in his investment account.

Now how’s that for motivation to start investing early for a young high school student!

#2 Basic Knowledge of the Stock Market

If I were to ask you what the stock market is, what would you say?

Is it the economy? Is it a get-rich-quick scheme? Is it a zero-sum game that should be avoided at all costs?

No, no, and no.

There’s a lot of confusion as to what the stock market actually is. And I don’t think that every high schooler, or anybody for that matter, needs to know every detail about how the stock market works.

But I do think that a little bit of education as to what the stock market is, and more importantly what it isn’t, would go a long way in helping people stick to their investment plan.

So what actually is the stock market? Well, let’s start by defining what a stock is.

A stock is a representation of ownership in a real company.

Look around you right now. Are you reading this on a MacBook, or maybe on a Dell PC? Both Apple and Dell are real companies that you can buy stock in.

Are you sipping on a latte from Starbucks right now? Starbucks is also a real company that you can buy stock in.

How does that apply to you? Well if you buy stock in Apple or Dell or Starbucks then you are a partial owner of Apple or Dell or Starbucks. Pretty cool, huh?

What does that mean for you? Well, as Apple sells more and more iPhones and MacBooks, and as Starbucks sells more and more coffee, their revenue continues to go up.

As their revenue goes up, the value of the company generally goes up too.

As the value of the company goes up, the value of your percentage ownership (based on the stock you own in the company) goes up. Get the picture?

So back to the question – “what is a stock market”.

A stock market is a place where people come to buy or sell stocks. Typically though, when people refer to the stock market they’re really asking “are the prices of companies generally going up or are they going down?”

Well, different company stock prices do different things in a day, so there’s what’s called a stock market index. And there’s many of these.

Take the S&P 500 for example. The S&P 500 gives is an index of 500 of the biggest companies in America (think Nike, Starbucks, General Electric). To oversimplify it just a bit, the price change of the S&P 500 just tells us whether, on average, the value of those 500 companies is going up or going down.

Why is it important to know that?

Because when you invest in something that, on average, drops in value by about 30% once every five years or so, the only thing that’s going to stop you from selling your investments at that point is an understanding of what you’re investing in.

If you just think of the stock market as a big gamble then there’s nothing to stop you from selling your stock market investments when they drop rapidly in value.

There’s no telling if you’ll lose everything, so you might as well cut your losses. Or at least that’s how the reasoning goes.

If, on the other hand, you understand that you are invested in real companies that make real products for real people, then you understand that an investment in a stock market index can only go to zero if every company that you own goes out of business. Is that possible?

Yes, anything is possible.

But is it likely? I’ll let you be the judge of that.

Bottom line is this – when you’re investing in the “stock market” you aren’t just owning something that changes value arbitrarily. You are owning real companies, and as those real companies become more valuable and more productive you get to participate in their growth.

Understanding this is a key component of actually achieving good investment results over time.

#3 How to Create a Budget

Ok, I know. What high schooler really wants to learn how to create a budget? I’m going to go out on a limb and say exactly 0% of them.

But can we all remember how clueless we were when we got our first real job paycheck and had absolutely no idea what to do with it?

Basic budgeting skills should start with an understanding of knowing what expenses you’ll have in a month. You should know how much each month needs to be spent on things like utilities, groceries, and insurance, while still making sure there’s enough to save.

Knowing these expenses will allow you to see how much is left over for discretionary spending.

Learning how to create a plan for your money is one of the most important skills that anyone can have.

It is the foundation that gives us the ability to save and invest like we would like.

#4 The Difference Between Good Debt and Bad Debt

In a perfect world, we wouldn’t ever have any debt. But there is a difference between good debt and bad debt.

What are some examples of “good” debt –

Mortgage debt that you use to purchase a home that you can afford.

NOTE – Here are two things that afford does NOT mean

- Mortgage payment that is less than your take-home income each month.

- The amount of mortgage that you are approved for.

You will almost always be approved for a larger mortgage than you can afford. Don’t fall into the trap of confusing approval with affordability.

Try to have your total monthly home payment (principal and interest portion of your mortgage, property taxes, insurance, HOA fees) come out to 30% of your take-home pay or less.

Too much higher than this and you run the risk of having a home payment that takes away your ability to save for other goals or spend as much as you would like each month.

Of course, this is easier to do in parts of the country where home prices are lower than they are in bigger metropolitan areas like San Diego, San Francisco, or New York. But you know what else is tough? Not having enough money each month to do what you want because your mortgage consumes all of your income.

Taking out a loan to start a business can also be good debt. Investing in your own business could be the best investment you ever make. But you need to make sure that this is a business that you believe in. Because if your business doesn’t make it that doesn’t mean that your loan just magically disappears.

What are some examples of bad debt –

Debt that you use to purchase a home you can’t afford.

See the analysis above.

Keep your home payment manageable so that you have the freedom to pursue other goals in addition to homeownership.

Credit card debt. More on this below.

Car loans for a car that you don’t need. Understand the difference between want and need here.

Yes, you need a car so that you can get to work and run your errands. No, you don’t need a new BMW 5 series unless you’re making enough income to support it.

I know your neighbor down the street has one and you want to be cool like them. Keep this in mind next time you drive by their house – they probably can’t afford it either!

#5 How Credit Cards Work

We all know how easy it is to go swipe a little piece of plastic at the grocery store and then magically our groceries are paid for. It might seem like free money to someone just getting started with their own card. But what is actually happening behind the scenes?

When you charge your credit card, the bank that it issues the card for you is essentially putting up money (i.e. extending credit) on your behalf. No money actually comes out of your account at the time, but you do begin building a credit balance that your bank is going to expect for you to pay back at the end of the month.

If managed correctly, credit cards can help young people to build credit over time. But there are some key points that everyone needs to know before using credit cards:

- You do have to pay back every dollar that you spend on your card. Go figure! As obvious as this seems, it’s tempting to put things we can’t afford on our credit cards. Instead, you should look to save up for what you want and only use credit cards for items that you can pay off in full each month.

- It does not help to carry a balance on your credit card. It is a popular misconception that carrying a balance helps build credit, but it’s wrong! Carrying a balance costs you a lot in interest and doesn’t help you build credit.

- Credit card interest is expensive! For any amount not paid in full expect to pay somewhere between 16% – 24% in interest. So don’t charge more on your credit card than you know you can pay off.

Credit card debt is the easiest type of debt to fall into and it’s also usually the most expensive type of debt.

In fact, in many cases, it may be better not to use a credit card at all. Studies show that using credit cards tends to dull the pain of buying, and that causes us to spend more than we otherwise would have.

The key to success with credit cards is understanding how they work and then understanding how to keep our behavior in check to avoid overspending.

Conclusion

So if you’re reading this and you have a child in high school, consider this: The Pythagorean Theorem is great. I love that A squared plus A squared equals C squared. But how much more will the principles outlined above help to prepare your high schooler for financial success?

Personal finance is important! Let’s treat it as such and prepare our students for success in their finances.